Source: Payments Cards and Mobile

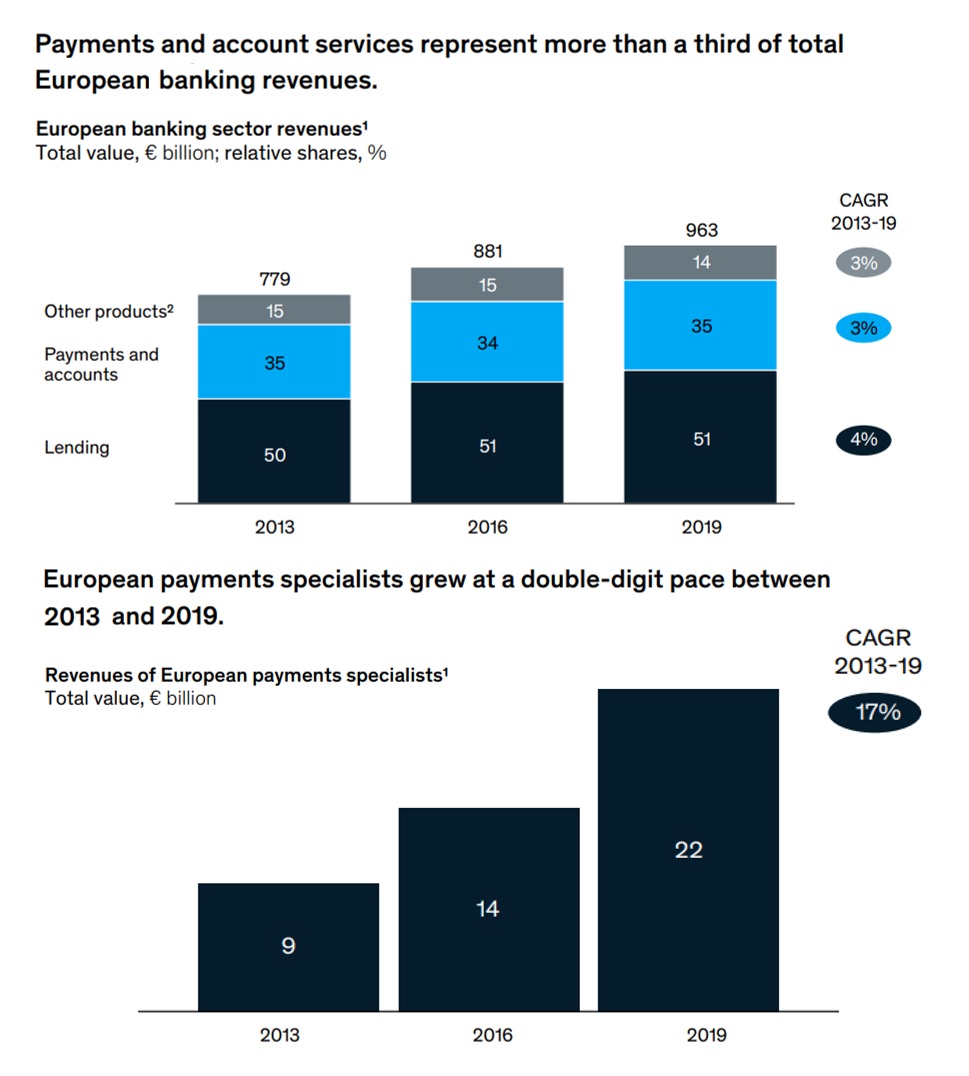

Payments and accounts services are at the core of banks’ offering to customers. They contributed about a third of European banks’ total revenues in 2019, and represent banks’ leading source of customer interactions, but these revenues are being rapidly eroded by 3rd party specialists.

Banks’ payments revenues have grown steadily at about 3% per year over the past six years. However, some specialist payments providers—processors, acquirers, schemes, and others—have achieved double-digit growth rates over the same period.

This suggests that banks’ traditional role at the centre of the payments ecosystem may be coming under challenge.

High ambitions, significant challenges

Almost two-thirds of the executives and experts who were surveyed as part of the The future of European payments:

Almost two-thirds of the executives and experts who were surveyed as part of the The future of European payments:

Strategic choices report for banks believe that banks will continue to be the leading players in European payments over the next five years.

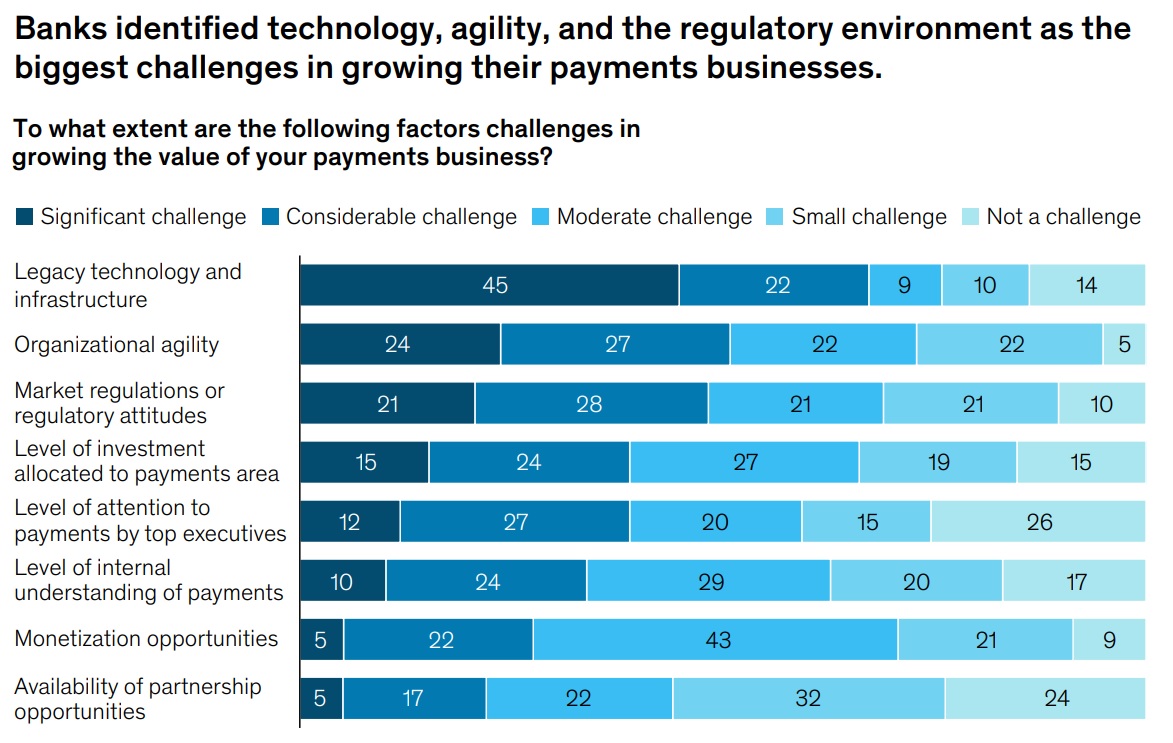

However, survey respondents and interviewees identified a number of challenges faced by banks.

These included increasing competition (especially from tech companies and FinTechs), the rise of technologies that could allow other providers to come between banks and their customer relationships, the lack of flexibility in banks’ operating models, the constrained revenue environment, rising customer expectations, and the complex regulatory outlook.

Executives also identified gaps in the capabilities and practices needed to grow their payments business, especially in technology, organisational agility, and monetisation models.

The effects of the pandemic

According to McKinsey’s Global Payments Map, the COVID-19 pandemic is likely to cause a temporary fall of about 6% in European payments revenues in 2020, followed by a rebound.

Fee-dependent revenues may recover more rapidly than interest-dependent revenues, although these had less room for decline given the long term compression of net interest margins in Europe.

Further fuel for a rebound may come from an acceleration in electronic payments in southern and eastern Europe as these regions catch up with digital migration in the north and west.

Many of the executives interviewed observed that the crisis had prompted them not to change the direction of their business but to reinforce their commitment to digitising customer journeys, introducing machine learning, and improving their technological and operational resilience.

Strengths and opportunities for banks

Interviewees noted that banks possess considerable strengths in payments, including access to large customer pools, control of current accounts and customer data, and balance sheets that allow them to provide liquidity for consumer lending, working capital financing, and corporate transaction management.

Interviewees also commented on banks’ opportunities to accelerate growth in digital payments, use real-time payments infrastructure to offer fully digitised customer experiences, and improve the flexibility and cost of their operating models by using application programming interfaces (APIs), offering payments-as-a-service (PaaS), and setting up industry utilities to build scale.

Many of the executives interviewed spoke of efforts to upgrade customer value propositions and optimise operating models, and some identified a need to adapt business models to changing industry dynamics.

Given the number and scale of the challenges, however, it remains to be seen whether banks’ efforts will go far enough to enable them to capture emerging market opportunities and grow the value of their businesses.

The outlook for the payments sector

On the stock markets, payments specialists outperformed the overall European banking sector between January and November 2020, with a shallower decline and a bigger rebound.

Interviewees noted that banks continue to be affected by mounting credit losses and low interest rates; payments specialists stand to gain from the shift to digital commerce and electronic payments; FinTechs have opportunities to target a broader pool of customers and capitalise on their cost advantages.

But are more exposed to structural factors because of the narrower focus of their customer relationships; and big tech companies have ample resources to invest but may come under increased scrutiny from governments and regulators.

Despite the uncertainties, the interviewees saw the outlook for payments as broadly positive. Most felt the crisis of 2020 would not damage their strategic position, and could even improve it.

The strategic choices facing banks In defining their strategy for each customer segment and step in the payments value chain, banks can choose to lead, accelerate, follow, or reduce their payments footprint, depending on their wider aspirations and starting point.

Leading requires banks to set ambitious goals, capitalise on strong capabilities, and invest at scale in payments as a means of competitive differentiation. All the banks interviewed aspired to lead in at least one customer segment.

Accelerating could involve making standalone investments; partnering to gain scale, expand customer access, and reduce time to market; or forming industry coalitions to address customer pain points and build new propositions. About half of the banks interviewed intended to accelerate in consumer payments.

Following is an option for a bank seeking to provide payments products and services without investing substantial resources. Some banks are already tacitly following this strategy in segments that require high scale or are strongly contested by specialists and tech companies.

Reducing the payments footprint can be achieved through the use of partners for selected activities and applications. Banks have a range of opportunities to collaborate with other organisations to fill capability gaps, drive economies of scale, mitigate investment risk, reduce the complexity of providing non-differentiating activities, and help set new market standards.

All the banks interviewed believed that cooperation is extremely important and were willing to pursue collaborations in the future.

What’s next for payments?

As technological advances, evolving customer behaviour, new market dynamics, and changing regulatory agendas converge with the after effects of the pandemic, the early 2020s may become an inflection point for payments.

Despite the uncertainties of the current environment, this could be the moment for banks to secure the growth of value in their payments business over the next cycle—and to come together with other stakeholders to solve sector-wide challenges and capture opportunities.

Categories: ATMs Banking